Price a Swaption Using SABR Model and Analytic Pricer

This example shows how to price a swaption using the SABR model. First, you construct a swaption volatility surface from market volatilities by calibrating the SABR model parameters separately for each swaption maturity using the SABR analytic pricer. You then compute the swaption price by using the implied Black volatility on the surface with the SABR analytic pricer.

Step 1. Load market swaption volatility data.

Load the zero curve and market implied Black volatility data for swaptions.

Settle = datetime(2013, 6, 14); ZeroDates = Settle + [calmonths([1 3 6]) calyears([1 2 3 4 5 6 7 8 9 10 12 15 20])]'; ZeroRates = [0.22 0.31 0.45 0.73 0.54 0.72 1.22 1.54 1.83 1.92 ... 2.16 2.32 2.52 2.93 3.12 3.36]'/100; ZeroCurve = ratecurve("zero",Settle,ZeroDates,ZeroRates,'Compounding',1); ExerciseDates = Settle + [calmonths(3) calyears([1 2 3 4 5 7 10])]'; YearsToExercise = yearfrac(Settle,ExerciseDates,1); NumMaturities = length(YearsToExercise); MarketVolatilities = [ ... 56.5 52.7 49.1 44.9 43.5 40.5 34.8 32.2 45.8 46.2 44.2 41.1 39.1 36.1 33.2 31.3 34.7 38.8 39.0 37.2 36.8 33.2 30.1 28.1 33.9 35.9 36.9 35.8 34.2 30.5 29.0 27.0 40.8 41.2 38.6 37.0 35.3 32.0 29.5 26.5 45.1 42.8 41.2 38.3 37.2 33.2 30.3 27.2 50.2 45.4 43.2 39.9 38.0 34.1 31.5 28.3]/100; MarketStrikes = [ ... 1.02 1.31 1.78 2.08 2.21 2.34 2.60 2.69; 1.52 1.81 2.28 2.58 2.71 2.84 3.10 3.19; 2.02 2.31 2.78 3.08 3.21 3.34 3.60 3.69; 2.52 2.81 3.28 3.58 3.71 3.84 4.10 4.19; 3.02 3.31 3.78 4.08 4.21 4.34 4.60 4.69; 3.52 3.81 4.28 4.58 4.71 4.84 5.10 5.19; 4.02 4.31 4.78 5.08 5.21 5.34 5.60 5.69]/100; CurrentForwardValues = MarketStrikes(4,:)

CurrentForwardValues = 1×8

0.0252 0.0281 0.0328 0.0358 0.0371 0.0384 0.0410 0.0419

ATMVolatilities = MarketVolatilities(4,:)

ATMVolatilities = 1×8

0.3390 0.3590 0.3690 0.3580 0.3420 0.3050 0.2900 0.2700

The current underlying forward rates and the corresponding at-the-money volatilities across the eight swaption maturities are represented in the fourth rows of the two matrices.

Step 2. Calibrate the SABR model parameters for each swaption maturity.

When you use a static SABR model, where the model parameters are assumed to be constant with respect to time, the parameters are calibrated separately for each swaption maturity (years to exercise) in a for loop using the SABR analytic pricer. To better represent market at-the-money volatilities, the Alpha parameter values are implied by the market at-the-money volatilities (for details, see Method 2 in Calibrate SABR Model Using Analytic Pricer).

% Define the predetermined Beta, calibrate SABR model parameters for each % swaption maturity, and display the calibrated parameters in a table. Beta = 0.5; Betas = repmat(Beta, NumMaturities, 1); Alphas = zeros(NumMaturities, 1); Rhos = zeros(NumMaturities, 1); Nus = zeros(NumMaturities, 1); options = optimoptions('lsqnonlin','Display','none'); for k = 1:NumMaturities % This function solves the SABR at-the-money volatility equation as a % polynomial of Alpha. alpharoots = @(Rho,Nu) roots([... (1 - Beta)^2*YearsToExercise(k)/24/CurrentForwardValues(k)^(2 - 2*Beta) ... Rho*Beta*Nu*YearsToExercise(k)/4/CurrentForwardValues(k)^(1 - Beta) ... (1 + (2 - 3*Rho^2)*Nu^2*YearsToExercise(k)/24) ... -ATMVolatilities(k)*CurrentForwardValues(k)^(1 - Beta)]); % This function converts at-the-money volatility into Alpha by picking the % smallest positive real root. atmVol2SabrAlpha = @(Rho,Nu) min(real(arrayfun(@(x) ... x*(x>0) + realmax*(x<0 || abs(imag(x))>1e-6), alpharoots(Rho,Nu)))); % Fit Rho and Nu (while converting at-the-money volatility into Alpha). objFun = @(X) MarketVolatilities(:,k) - ... volatilities(finpricer("Analytic", 'Model', finmodel("SABR", ... 'Alpha', atmVol2SabrAlpha(X(1), X(2)), 'Beta', Beta, 'Rho', X(1), 'Nu', X(2)), ... 'DiscountCurve', ZeroCurve), ExerciseDates(k), CurrentForwardValues(k), MarketStrikes(:,k)); X = lsqnonlin(objFun, [0 0.5], [-1 0], [1 Inf], options); Rho = X(1); Nu = X(2); % Get final Alpha from the calibrated parameters. Alpha = atmVol2SabrAlpha(Rho, Nu); Alphas(k) = Alpha; Rhos(k) = Rho; Nus(k) = Nu; end CalibratedParameters = array2table([Alphas Betas Rhos Nus], ... 'VariableNames',{'Alpha' 'Beta' 'Rho' 'Nu'}, ... 'RowNames',{'3M into 10Y';'1Y into 10Y'; ... '2Y into 10Y';'3Y into 10Y';'4Y into 10Y'; ... '5Y into 10Y';'7Y into 10Y';'10Y into 10Y'})

CalibratedParameters=8×4 table

Alpha Beta Rho Nu

________ ____ ________ _______

3M into 10Y 0.051895 0.5 0.40869 1.4054

1Y into 10Y 0.054381 0.5 0.28066 1.1234

2Y into 10Y 0.057325 0.5 0.2166 0.97407

3Y into 10Y 0.057243 0.5 0.19837 0.82932

4Y into 10Y 0.053387 0.5 0.17304 0.81441

5Y into 10Y 0.04673 0.5 0.11618 0.80138

7Y into 10Y 0.046986 0.5 0.1554 0.63377

10Y into 10Y 0.04443 0.5 0.080169 0.52515

Step 3. Construct a volatility surface.

Use the calibrated SABR model to compute new volatilities at any strike value to produce a smooth smile for a given maturity. This can be repeated for each maturity to form a volatility surface.

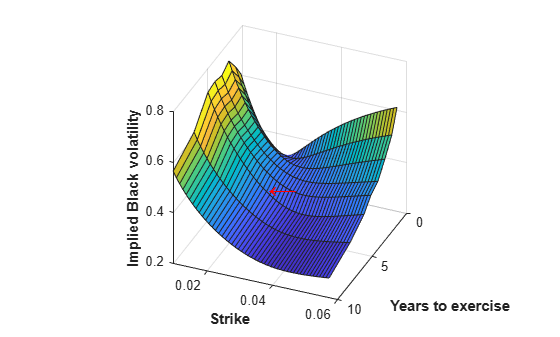

Compute volatilities using the calibrated models for each maturity and plot the volatility surface.

PlottingStrikes = (0.95:0.1:5.8)'/100; ComputedVols = zeros(length(PlottingStrikes), NumMaturities); for k = 1:NumMaturities SABRModel = finmodel("SABR", ... 'Alpha', Alphas(k), 'Beta', Betas(k), 'Rho', Rhos(k), 'Nu', Nus(k)); ComputedVols(:,k) = volatilities(finpricer("Analytic", ... 'Model', SABRModel, 'DiscountCurve', ZeroCurve), ... ExerciseDates(k), CurrentForwardValues(k), PlottingStrikes); end figure; surf(YearsToExercise, PlottingStrikes, ComputedVols); xlim([0 10]); ylim([0.0095 0.06]); zlim([0.2 0.8]); view(113,32); set(gca, 'Position', [0.13 0.11 0.775 0.815], ... 'PlotBoxAspectRatioMode', 'manual'); xlabel('Years to exercise', 'Fontweight', 'bold'); ylabel('Strike', 'Fontweight', 'bold'); zlabel('Implied Black volatility', 'Fontweight', 'bold');

Note that in this volatility surface, the smiles tend to get flatter for longer swaption maturities (years to exercise). This is consistent with the Nu parameter values tending to decrease with swaption maturity, as shown in the table for CalibratedParameters.

Step 4. Use the SABR analytic pricer to price a swaption.

Use the SABR analytic pricer to price a swaption that matures in five years. First, create the underlying 10-year swap instrument starting in five years and create the Swaption instrument for this underlying Swap. Then create the SABR model for this swaption maturing in five years, which is used for creating the SABR analytic pricer.

% Create the underlying 10-year swap starting in 5 years. MaturityIdx = 6; SwapStartDate = ExerciseDates(MaturityIdx); SwapMaturity = SwapStartDate + calyears(10); Swap = fininstrument("Swap", 'Maturity', SwapMaturity, ... 'LegRate', [0 0], "LegType",["fixed" "float"],... "ProjectionCurve", ZeroCurve, "StartDate", SwapStartDate)

Swap =

Swap with properties:

LegRate: [0 0]

LegType: ["fixed" "float"]

Reset: [2 2]

Basis: [0 0]

Notional: 100

LatestFloatingRate: [NaN NaN]

ResetOffset: [0 0]

DaycountAdjustedCashFlow: [0 0]

ProjectionCurve: [1×2 ratecurve]

BusinessDayConvention: ["actual" "actual"]

Holidays: NaT

EndMonthRule: [1 1]

StartDate: 14-Jun-2018

Maturity: 14-Jun-2028

Name: ""

% Create the swaption (for the underlying 10-year swap) maturing in five % years. SwaptionExerciseDate = SwapStartDate; Reset = 1; OptSpec = 'call'; Strike = 0.0272; Swaption = fininstrument("Swaption", 'Strike', Strike, ... 'ExerciseDate', SwaptionExerciseDate, 'Swap', Swap, 'OptionType', OptSpec)

Swaption =

Swaption with properties:

OptionType: "call"

ExerciseStyle: "european"

ExerciseDate: 14-Jun-2018

Strike: 0.0272

Swap: [1×1 fininstrument.Swap]

Name: ""

% Create the SABR model for the swaption maturing in five years. SABRModel = finmodel("SABR", ... 'Alpha', Alphas(MaturityIdx), 'Beta', Betas(MaturityIdx), ... 'Rho', Rhos(MaturityIdx), 'Nu', Nus(MaturityIdx))

SABRModel =

SABR with properties:

Alpha: 0.0467

Beta: 0.5000

Rho: 0.1162

Nu: 0.8014

Shift: 0

VolatilityType: "black"

% Create the SABR analytic pricer. SABRPricer = finpricer("Analytic", 'Model', SABRModel, 'DiscountCurve', ZeroCurve)

SABRPricer =

SABR with properties:

DiscountCurve: [1×1 ratecurve]

Model: [1×1 finmodel.SABR]

To visualize the SABR implied Black volatility used in pricing the swaption, first compute the current forward swap rate by using the parswaprate function.

CurrentForwardSwapRate = parswaprate(Swap,ZeroCurve)

CurrentForwardSwapRate = 0.0384

Next, compute the SABR implied Black volatility for this Swaption by using the volatilities function, and it is marked with a red arrow in the figure at the bottom.

SABRBlackVolatility = volatilities(SABRPricer, ...

SwaptionExerciseDate, CurrentForwardSwapRate, Strike)SABRBlackVolatility = 0.3665

text (YearsToExercise(MaturityIdx), Strike, SABRBlackVolatility, ... '\leftarrow', 'Color', 'r', 'FontWeight', 'bold', 'FontSize', 22);

Finally, price the swaption using the price function of the SABR analytic pricer.

SwaptionPrice = price(SABRPricer, Swaption)

SwaptionPrice = 13.0141

References

[1] Hagan, Patrick S., Deep Kumar, Andrew S. Lesniewski, and Diana E. Woodward. "Managing Smile Risk." Wilmott Magazine. (January 2002): 84–108.

[2] West, Graeme. "Calibration of the SABR Model in Illiquid Markets." Applied Mathematical Finance. 12, no. 4 (December 2005): 371–385.