Analyzing Financial Time-Series Using Random Matrix Theory

Duan Wang, SLC Management

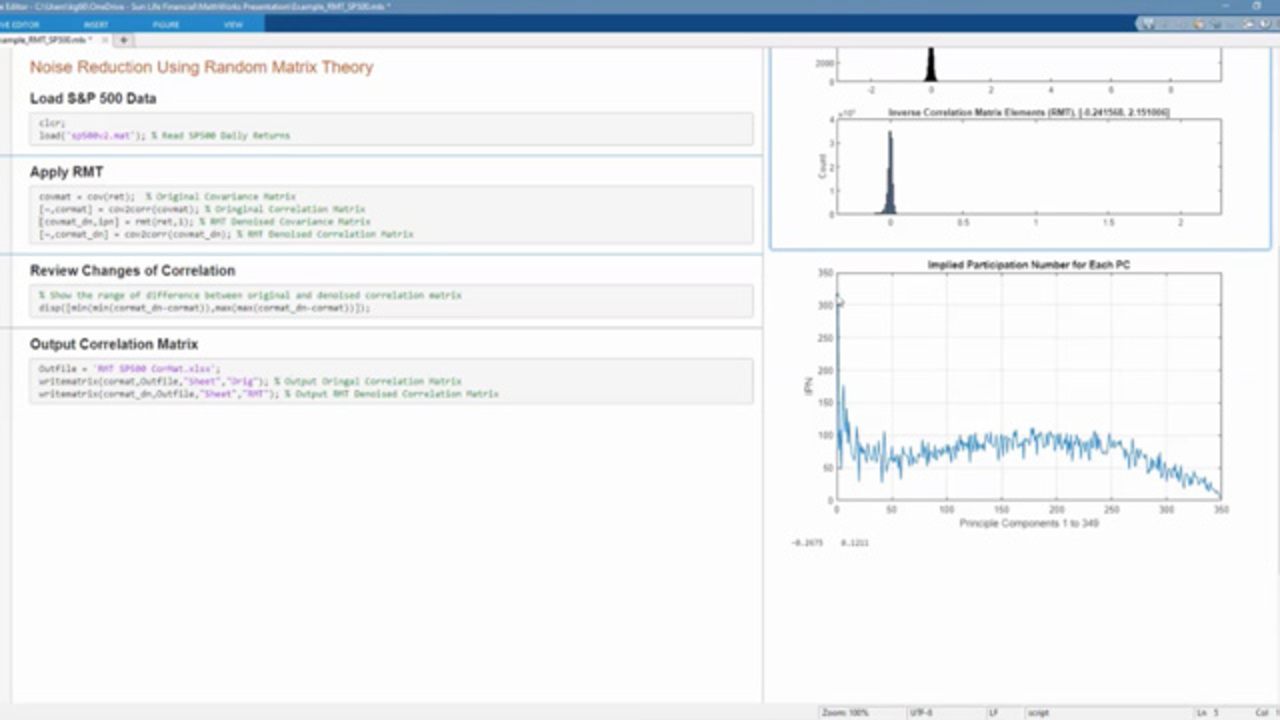

Random matrix theory (RMT) is a useful tool for noise reduction in the sample covariance matrix in financial time-series analysis. Duan Wang, a quantitative analyst on the Derivatives and Quantitative Strategies team, demonstrates how SLC Management implemented RMT in MATLAB® to produce an improved estimator for the sample covariance variance. He also shows a couple of examples in portfolio optimization and asset allocation.

Published: 14 Nov 2022

Featured Product

MATLAB

Up Next:

Related Videos:

Seleccione un país/idioma

Seleccione un país/idioma para obtener contenido traducido, si está disponible, y ver eventos y ofertas de productos y servicios locales. Según su ubicación geográfica, recomendamos que seleccione: United States.

También puede seleccionar uno de estos países/idiomas:

América

- América Latina (Español)

- Canada (English)

- United States (English)

Europa

- Belgium (English)

- Denmark (English)

- Deutschland (Deutsch)

- España (Español)

- Finland (English)

- France (Français)

- Ireland (English)

- Italia (Italiano)

- Luxembourg (English)

- Netherlands (English)

- Norway (English)

- Österreich (Deutsch)

- Portugal (English)

- Sweden (English)

- Switzerland

- United Kingdom (English)