simulate

Monte Carlo simulation of univariate regression model with ARIMA time series errors

Syntax

Description

Y = simulate(Mdl,numobs,Name=Value)simulate returns numeric arrays when all optional input data are

numeric arrays. For example, simulate(Mdl,10,NumPaths=1000,X=Pred)

simulates 1000 sample paths of length 10 from the

regression model with ARIMA errors Mdl, and uses the predictor data in

Pred for the model regression component.

Tbl = simulate(Mdl,numobs,Presample=Presample,PresampleInnovationVariable=PresampleInnovationVariable)Tbl containing a variable for each of

the random paths of response, error model innovation, and unconditional disturbance series

resulting from simulating the regression model with ARIMA errors Mdl.

simulate uses the error model variable

PresampleInnovationVariable in the table or timetable of presample

data Presample to initialize the model. (since R2023b)

To initialize the model using presample unconditional disturbance data, replace the

PresampleInnovationVariable name-value argument with

PresampleRegressionDisturbanceVariable name-value argument.

Tbl = simulate(Mdl,numobs,InSample=InSample,PredictorVariables=PredictorVariables)PredictorVariables in the in-sample table or

timetable of data InSample containing the predictor data for the

model regression component. (since R2023b)

Tbl = simulate(Mdl,numobs,Presample=Presample,PresampleInnovationVariable=PresampleInnovationVariable,InSample=InSample,PredictorVariables=PredictorVariables)

Tbl = simulate(___,Name=Value)

For example,

simulate(Mdl,100,NumPaths=1000,InSample=Tbl,PredictoreVariables="CPI")

returns a timetable containing a variable for each of the response, error model

innovation, and unconditional disturbance series. Each variable is a 100-by-1000 matrix

representing 1000, 100-period paths simulated from the regression model with ARIMA errors.

simulate applies the predictor data in the

CPI variable of the timetable Tbl to the model

regression component.

Examples

Create the following regression model with ARMA(2,1) errors:

where is Gaussian with variance 0.1.

Mdl = regARIMA(Intercept=1,AR={0.5 -0.8},MA=-0.5, ...

Variance=0.1);Mdl is a fully specified regARIMA object.

Simulate a path of responses of length 100.

rng(1,"twister") % For reproducibility y = simulate(Mdl,100);

y is a 100-by-1 vector containing the response path simulated from Mdl.

Plot the simulated path.

plot(y)

Simulate 1000 paths of responses from the following regression model with ARMA(2,1) errors:

where is Gaussian with variance 0.1. Assume the predictors are standard Gaussian random variables. Provide data as numeric arrays.

Create the regression model with ARIMA errors.

Mdl = regARIMA(Intercept=0,AR={0.5 -0.8},MA=-0.5, ...

Beta=[0.1; -0.2],Variance=0.1);Simulate two series of predictor data for the regression component.

rng(1,"twister") % For reproducibility Pred = randn(100,2);

Simulate 1000 paths of responses each of length 100.

numobs = 100; numpaths = 1000; y = simulate(Mdl,100,X=Pred,NumPaths=1000);

y is a 1000-by-100 matrix containing the independent response paths simulated from Mdl.

Plot the simulated paths.

plot(y)

Simulate paths of responses, innovations, and unconditional disturbances from a regression model with SARIMA errors.

Specify the model:

where follows a t-distribution with 15 degrees of freedom.

dstr = struct("Name","t","DoF",15); Mdl = regARIMA(AR={0.2 0.1},MA=0.5,SAR=0.01,SARLags=12, ... SMA=0.02,SMALags=12,D=1,Seasonality=12,Beta=[1.5; -2], ... Intercept=0,Variance=0.1,Distribution=dstr)

Mdl =

regARIMA with properties:

Description: "Regression with ARIMA(2,1,1) Error Model Seasonally Integrated with Seasonal AR(12) and MA(12) (t Distribution)"

SeriesName: "Y"

Distribution: Name = "t", DoF = 15

Intercept: 0

Beta: [1.5 -2]

P: 27

D: 1

Q: 13

AR: {0.2 0.1} at lags [1 2]

SAR: {0.01} at lag [12]

MA: {0.5} at lag [1]

SMA: {0.02} at lag [12]

Seasonality: 12

Variance: 0.1

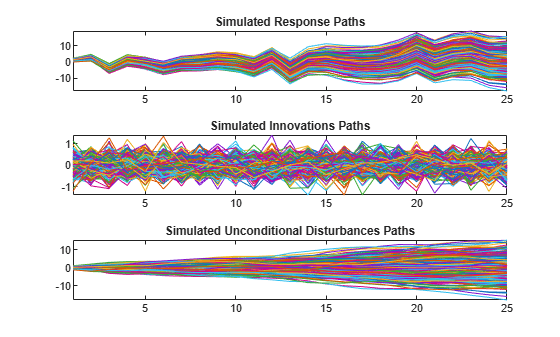

Simulate and plot 500 paths with 25 observations each.

T = 25; rng(1,"twister") % For reproducibility Pred = randn(T,2); [Y,E,U] = simulate(Mdl,T,NumPaths=500,X=Pred); figure tiledlayout(3,1) nexttile plot(Y) axis tight title("Simulated Response Paths") nexttile plot(E) axis tight title("Simulated Innovations Paths") nexttile plot(U) axis tight title("Simulated Unconditional Disturbances Paths")

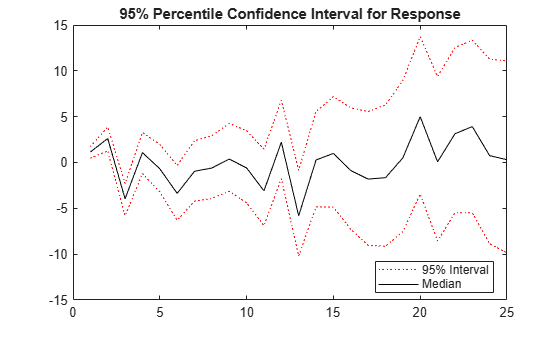

Plot the 2.5th, 50th (median), and 97.5th percentiles of the simulated response paths.

lower = prctile(Y,2.5,2); middle = median(Y,2); upper = prctile(Y,97.5,2); figure plot(1:25,lower,"r:",1:25,middle,"k",1:25,upper,"r:") title("95% Percentile Confidence Interval for Response") legend("95% Interval","Median",Location="best")

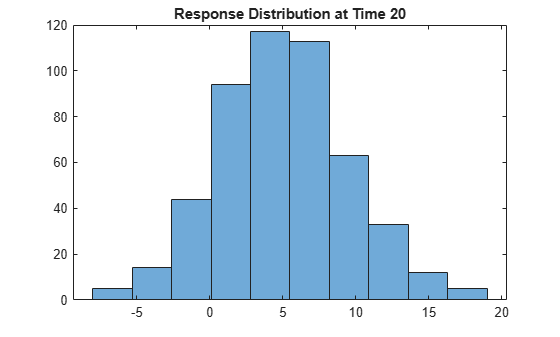

Compute statistics across the second dimension (across paths) to summarize the sample paths.

Plot a histogram of the simulated paths at time 20.

figure

histogram(Y(20,:),10)

title("Response Distribution at Time 20")

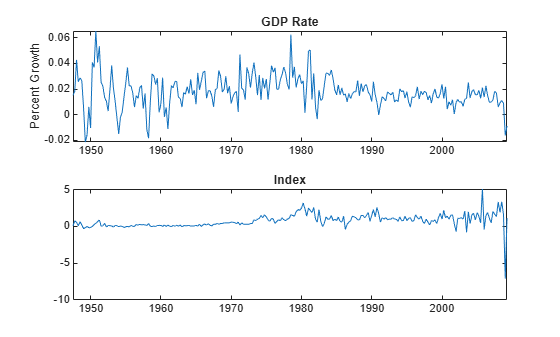

Fit a regression model with ARMA(1,1) errors by regressing the US consumer price index (CPI) quarterly changes onto the US gross domestic product (GDP) growth rate. Forecast log GDP using Monte Carlo simulation and the estimated model. Supply data in timetables.

Load and Transform Data

Load the US macroeconomic data set. Compute the series of GDP quarterly growth rates and CPI quarterly changes.

load Data_USEconModel DTT = price2ret(DataTimeTable,DataVariables="GDP"); DTT.GDPRate = 100*DTT.GDP; DTT.CPIDel = diff(DataTimeTable.CPIAUCSL); T = height(DTT)

T = 248

figure tiledlayout(2,1) nexttile plot(DTT.Time,DTT.GDPRate) title("GDP Rate") ylabel("Percent Growth") nexttile plot(DTT.Time,DTT.CPIDel) title("Index")

The series appear stationary, albeit heteroscedastic.

Prepare Timetable for Estimation

When you plan to supply a timetable, you must ensure it has all the following characteristics:

The selected response variable is numeric and does not contain any missing values.

The timestamps in the

Timevariable are regular, and they are ascending or descending.

Remove all missing values from the timetable.

DTT = rmmissing(DTT); T_DTT = height(DTT)

T_DTT = 248

Because each sample time has an observation for all variables, rmmissing does not remove any observations.

Determine whether the sampling timestamps have a regular frequency and are sorted.

areTimestampsRegular = isregular(DTT,"quarters")areTimestampsRegular = logical

0

areTimestampsSorted = issorted(DTT.Time)

areTimestampsSorted = logical

1

areTimestampsRegular = 0 indicates that the timestamps of DTT are irregular. areTimestampsSorted = 1 indicates that the timestamps are sorted. Macroeconomic series in this example are timestamped at the end of the month. This quality induces an irregularly measured series.

Remedy the time irregularity by shifting all dates to the first day of the quarter.

dt = DTT.Time; dt = dateshift(dt,"start","quarter"); DTT.Time = dt; areTimestampsRegular = isregular(DTT,"quarters")

areTimestampsRegular = logical

1

DTT is regular.

Create Model Template for Estimation

Suppose that a regression model of the quarterly GDP rate on CPI changes, with ARMA(1,1) errors, is appropriate.

Create a model template for a regression model with ARMA(1,1) errors template. Specify the response variable name.

Mdl = regARIMA(1,0,1);

Mdl.SeriesName = "GDPRate";Mdl is a partially specified regARIMA object.

Partition Data

Reserve 2 years (8 quarters) of data at the end of the series to compare against the forecasts.

numobs = 8; estidx = 1:(T_DTT-numobs); % Estimation sample frstHzn = (T_DTT-numobs+1):T_DTT; % Forecast horizon

Fit Model to Data

Fit a regression model with ARMA(1,1) errors to the estimation sample. Specify the predictor variable name.

EstMdl = estimate(Mdl,DTT(estidx,:),PredictorVariables="CPIDel");

Regression with ARMA(1,1) Error Model (Gaussian Distribution):

Value StandardError TStatistic PValue

__________ _____________ __________ __________

Intercept 0.016489 0.0017307 9.5272 1.6152e-21

AR{1} 0.57835 0.096952 5.9653 2.4415e-09

MA{1} -0.15125 0.11658 -1.2974 0.19449

Beta(1) 0.0025095 0.0014147 1.7738 0.076089

Variance 0.00011319 7.5405e-06 15.01 6.2792e-51

EstMdl is a fully specified, estimated regARIMA object. By default, estimate backcasts for the required Mdl.P = 1 presample regression model residual and sets the required Mdl.Q = 1 presample error model residual to 0.

Forecast Estimated Model

Infer estimation sample unconditional disturbances to initialize the model for forecasting. Specify the predictor variable name.

Tbl0 = infer(EstMdl,DTT(estidx,:),PredictorVariables="CPIDel");Simulate 1000 paths with 8 observations each. Use the inferred unconditional disturbances as presample data. Specify the predictor and presample unconditional disturbance variable names.

rng(1,"twister"); % For reproducibility numpaths = 1000; TblSim = simulate(EstMdl,numobs,NumPaths=numpaths,Presample=Tbl0, ... PresampleRegressionDisturbanceVariable="GDPRate_RegressionResidual", ... InSample=DTT(frstHzn,:),PredictorVariables="CPIDel");

Plot the simulation median forecast and approximate 95% forecast intervals.

TblSim.FStats = quantile(TblSim.GDPRate_Response,[0.025 0.5 0.975],2); figure plot(DTT.Time(end-40:end),DTT.GDPRate(end-40:end),Color=[.7,.7,.7]) hold on h1 = plot(TblSim.Time,TblSim.FStats(:,[1 3]),"r:",LineWidth=2); h2 = plot(TblSim.Time,TblSim.FStats(:,2),"k",LineWidth=2); h = gca; ph = patch([repmat(TblSim.Time(1),1,2) repmat(TblSim.Time(end),1,2)], ... [h.YLim fliplr(h.YLim)], ... [0 0 0 0],"b"); ph.FaceAlpha = 0.1; legend([h1(1) h2],["95% percentile intervals" "Sim. median"],Location="northwest", ... AutoUpdate="off") axis tight title("GDP Rate Forecast Over 2-year Horizon") hold off

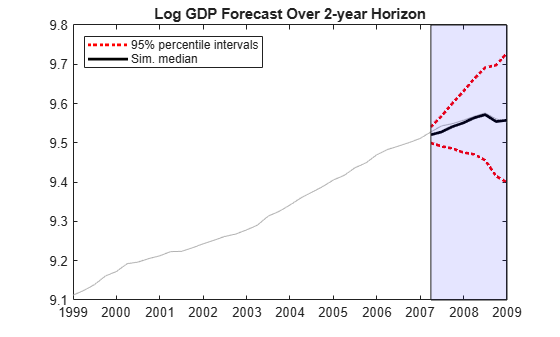

Fit a regression model with ARIMA(1,1,1) errors by regressing the quarterly log US GDP onto the log CPI. Forecast log GDP using Monte Carlo simulation and the estimated model. Supply data in timetables.

Load the US macroeconomic data set. Compute the log GDP series.

load Data_USEconModel

DTT = DataTimeTable;

DTT.LogGDP = log(DTT.GDP);

T = height(DTT);Remedy the time irregularity by shifting all dates to the first day of the quarter.

dt = DTT.Time; dt = dateshift(dt,"start","quarter"); DTT.Time = dt;

Reserve 2 years (8 quarters) of data at the end of the series to compare against the forecasts.

numobs = 8; estidx = 1:(T-numobs); % Estimation sample frstHzn = (T-numobs+1):T; % Forecast horizon

Suppose that a regression model of the quarterly log GDP on CPI, with ARMA(1,1) errors, is appropriate.

Create a model template for a regression model with ARMA(1,1) errors template. Specify the response variable name.

Mdl = regARIMA(1,1,1);

Mdl.SeriesName = "LogGDP";The intercept is not identifiable in a regression model with integrated errors. Fix its value before estimation. One way to do this is to estimate the intercept using simple linear regression. Use the estimation sample.

coeff = [ones(T-numobs,1) DTT.CPIAUCSL(estidx)]\DTT.LogGDP(estidx); Mdl.Intercept = coeff(1);

Fit a regression model with ARMA(1,1,1) errors to the estimation sample. Specify the predictor variable name.

EstMdl = estimate(Mdl,DTT(estidx,:),PredictorVariables="CPIAUCSL");

Regression with ARIMA(1,1,1) Error Model (Gaussian Distribution):

Value StandardError TStatistic PValue

__________ _____________ __________ ___________

Intercept 5.8303 0 Inf 0

AR{1} 0.92869 0.028414 32.684 2.6112e-234

MA{1} -0.39063 0.057599 -6.7819 1.1858e-11

Beta(1) 0.0029335 0.0014645 2.0031 0.045166

Variance 0.00010668 6.9256e-06 15.403 1.5539e-53

EstMdl is a fully specified, estimated regARIMA object. By default, estimate backcasts for the required Mdl.P = 2 presample regression model residual and sets the required Mdl.Q = 1 presample error model residual to 0.

Infer estimation sample unconditional disturbances to initialize the model for forecasting. Specify the predictor variable name.

Tbl0 = infer(EstMdl,DTT(estidx,:),PredictorVariables="CPIAUCSL");Simulate 1000 paths with 8 observations each. Use the inferred unconditional disturbances as presample data. Specify the predictor and presample unconditional disturbance variable names.

rng(1,"twister"); % For reproducibility numpaths = 1000; TblSim = simulate(EstMdl,numobs,NumPaths=numpaths,Presample=Tbl0, ... PresampleRegressionDisturbanceVariable="LogGDP_RegressionResidual", ... InSample=DTT(frstHzn,:),PredictorVariables="CPIAUCSL");

Plot the simulation median forecast and approximate 95% forecast intervals.

TblSim.FStats = quantile(TblSim.LogGDP_Response,[0.025 0.5 0.975],2); figure plot(DTT.Time(end-40:end),DTT.LogGDP(end-40:end),Color=[.7,.7,.7]) hold on h1 = plot(TblSim.Time,TblSim.FStats(:,[1 3]),"r:",LineWidth=2); h2 = plot(TblSim.Time,TblSim.FStats(:,2),"k",LineWidth=2); h = gca; ph = patch([repmat(TblSim.Time(1),1,2) repmat(TblSim.Time(end),1,2)], ... [h.YLim fliplr(h.YLim)],[0 0 0 0],"b"); ph.FaceAlpha = 0.1; legend([h1(1) h2],["95% percentile intervals" "Sim. median"],Location="northwest", ... AutoUpdate="off") axis tight title("Log GDP Forecast Over 2-year Horizon") hold off

Input Arguments

Name-Value Arguments

Output Arguments

References

[1] Box, George E. P., Gwilym M. Jenkins, and Gregory C. Reinsel. Time Series Analysis: Forecasting and Control. 3rd ed. Englewood Cliffs, NJ: Prentice Hall, 1994.

[2] Davidson, R., and J. G. MacKinnon. Econometric Theory and Methods. Oxford, UK: Oxford University Press, 2004.

[3] Enders, Walter. Applied Econometric Time Series. Hoboken, NJ: John Wiley & Sons, Inc., 1995.

[4] Hamilton, James D. Time Series Analysis. Princeton, NJ: Princeton University Press, 1994.

[5] Pankratz, A. Forecasting with Dynamic Regression Models. John Wiley & Sons, Inc., 1991.

[6] Tsay, R. S. Analysis of Financial Time Series. 2nd ed. Hoboken, NJ: John Wiley & Sons, Inc., 2005.

Version History

Introduced in R2013bSee Also

Objects

Functions

Topics

- Alternative ARIMA Model Representations

- Simulate Stationary Processes

- Simulate Trend-Stationary and Difference-Stationary Processes

- Monte Carlo Simulation of Conditional Mean Models

- Presample Data for Conditional Mean Model Simulation

- Transient Effects in Conditional Mean Model Simulations

- Forecast Conditional Mean Model Programmatically