mvtcdf

Multivariate t cumulative distribution function

Description

[

additionally returns an estimate of the error in p,err] = mvtcdf(___)p. For more

information, see Algorithms.

Examples

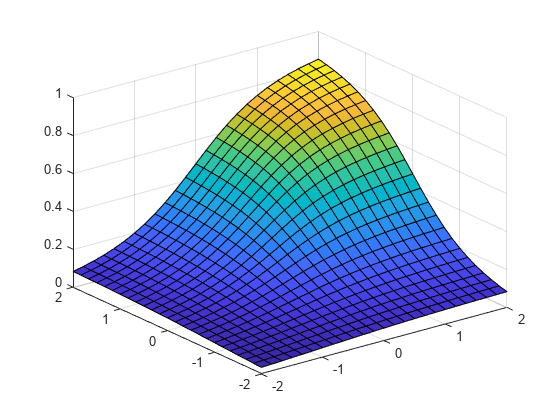

Compute the cdf of a multivariate t distribution with correlation the parameters C=[1 .4; .4 1] and 2 degrees of freedom.

C = [1 .4; .4 1]; df = 2; [X1,X2] = meshgrid(linspace(-2,2,25)',linspace(-2,2,25)'); X = [X1(:) X2(:)]; p = mvtcdf(X,C,df);

Plot the cdf.

figure; surf(X1,X2,reshape(p,25,25));

Input Arguments

Output Arguments

More About

Algorithms

For bivariate and trivariate distributions, the mvtcdf function uses

adaptive quadrature on a transformation of the t density, based on methods

developed by Genz [1]. The default absolute error tolerance for these cases is

1e-8. For four or more dimensions, the function uses a quasi-Monte Carlo

integration algorithm based on methods developed by Genz and Bretz [2]

[3]. The

default absolute error tolerance for these cases is 1e-4.

References

[1] Genz, A. “Numerical Computation of Rectangular Bivariate and Trivariate Normal and t Probabilities.” Statistics and Computing. Vol. 14, No. 3, 2004, pp. 251–260.

[2] Genz, A., and F. Bretz. “Numerical Computation of Multivariate t Probabilities with Application to Power Calculation of Multiple Contrasts.” Journal of Statistical Computation and Simulation. Vol. 63, 1999, pp. 361–378.

[3] Genz, A., and F. Bretz. “Comparison of Methods for the Computation of Multivariate t Probabilities.” Journal of Computational and Graphical Statistics. Vol. 11, No. 4, 2002, pp. 950–971.

Version History

Introduced in R2006a