Estadística

CLASIFICACIÓN

262

of 302.031

REPUTACIÓN

350

CONTRIBUCIONES

0 Preguntas

141 Respuestas

ACEPTACIÓN DE RESPUESTAS

0.00%

VOTOS RECIBIDOS

74

CLASIFICACIÓN

421 of 21.508

REPUTACIÓN

3.919

EVALUACIÓN MEDIA

4.60

CONTRIBUCIONES

12 Archivos

DESCARGAS

52

ALL TIME DESCARGAS

31301

CLASIFICACIÓN

of 178.295

CONTRIBUCIONES

0 Problemas

0 Soluciones

PUNTUACIÓN

0

NÚMERO DE INSIGNIAS

0

CONTRIBUCIONES

35 Publicaciones

CONTRIBUCIONES

0 Público Canales

EVALUACIÓN MEDIA

CONTRIBUCIONES

0 Temas destacados

MEDIA DE ME GUSTA

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Feeds

Publicado

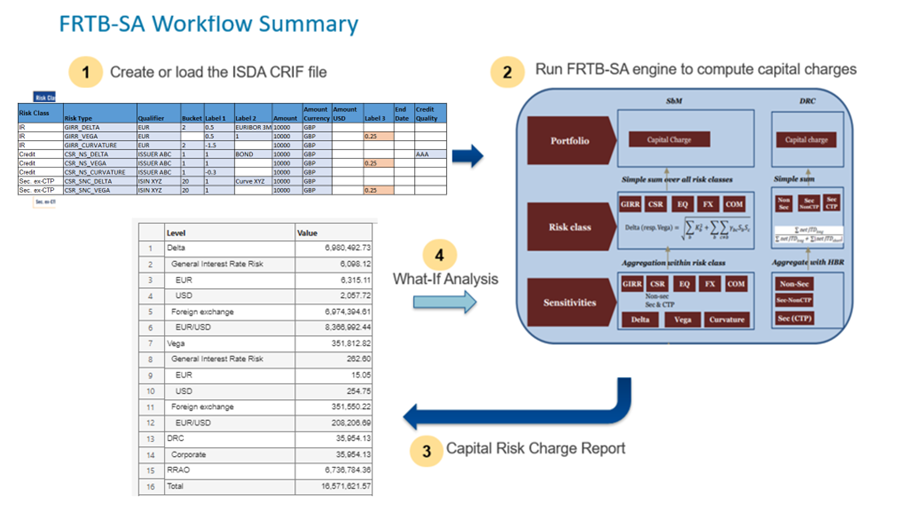

Navigating FRTB: Standardized vs Internal Models – and the Role of Scriptable Risk Engines

The Fundamental Review of the Trading Book (FRTB) is reshaping how banks measure and manage market risk. Beyond replacing...

11 meses hace

Publicado

The FRED Connector in Datafeed Toolbox

If you work with macro, markets, or policy analysis, chances are you touch FRED®—the Federal Reserve Economic Data service....

11 meses hace

Publicado

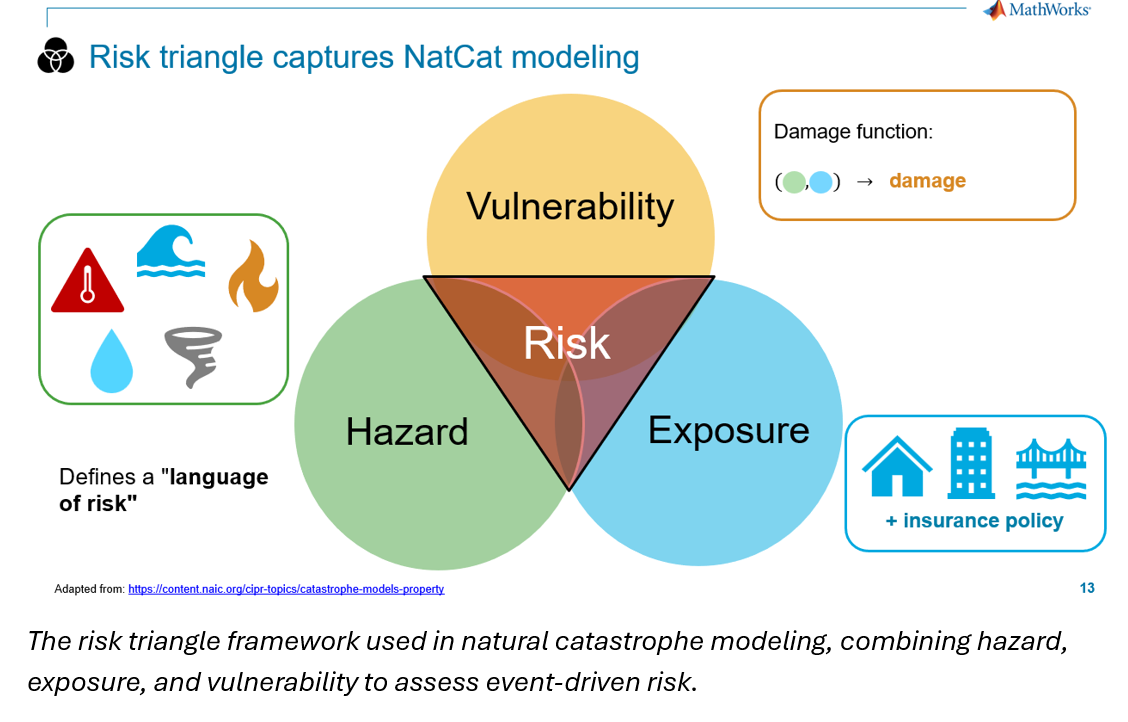

Analyzing the Financial Risks of Wildfires

We recently hosted a technical webinar focused on analyzing the financial risks of wildfires. Akshay Paul and Yuchen Dong...

11 meses hace

Publicado

Building a Neural Network for Time Series Forecasting – Low-Code Workflow

The following post is from Yuchen Dong, Senior Financial Application Engineer at MathWorks. Financial institutions forecast...

alrededor de 1 año hace

Publicado

GDP Nowcasting with MATLAB

What is GDP Nowcasting? Imagine trying to drive a car while only getting speed updates every three months. That’s kind of...

alrededor de 1 año hace

Publicado

Modeling Physical Climate Risk Across Financial Portfolios

Financial institutions are reassessing long-term risk models as physical climate events like hurricanes, floods, and...

alrededor de 1 año hace

Publicado

Accelerating Asset Management with ModelOps: From Model Building to Monitoring

Asset management quants face complex data environments, tight timelines, and the constant pressure to translate models into...

más de 1 año hace

Publicado

2nd Biennial Macroeconometric Caribbean Conference

MathWorks was recently invited to the 2nd Biennial Macroeconometric Caribbean Conference in Nassau, Bahamas, organized by...

más de 1 año hace

Publicado

The Economic Effects of Tariff Changes

The following post is from Yuchen Dong, Senior Financial Application Engineer. The code presented in this blog can be found...

más de 1 año hace

Publicado

Modeling Exchange Rate Volatility

The following post is from William Mueller, Software Developer on the Econometrics Toolbox Team. Forecasting currency...

más de 1 año hace

Publicado

Assessing Climate Impacts on Credit Risk

We recently hosted a technical webinar focused on climate transition risk, specifically assessing climate impacts on credit...

más de 1 año hace

Publicado

Simplifying Econometric Modeling with MATLAB

Econometric modeling is essential for analyzing economic data, making forecasts, and informing policy decisions, however,...

más de 1 año hace

Publicado

Celebrating 30 Years of Dynare and Its Global Impact with MATLAB

As we celebrate the 30th anniversary of Dynare, we at MathWorks would like to take a moment to reflect on its influence on...

más de 1 año hace

Publicado

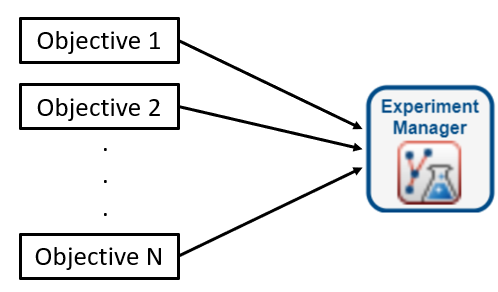

Custom Portfolio Optimization: Balancing Objectives, Constraints, and Efficiency

The following blog was written by Marshall Alphonso Principal Engineer and Sara Galante, Senior Finance Application...

más de 1 año hace

Publicado

Physics-Informed Neural Networks (PINNs) for Option Pricing

The following post is from Jue Liu from Columbia University and Yuchen Dong from MathWorks. The example featured in the...

más de 1 año hace

Publicado

MathWorks Secures Silver in Chartis RiskTech AI 50 and Excels in Key Categories

We are proud to announce that MathWorks has been ranked second overall in the inaugural Chartis RiskTech AI 50, an...

más de 1 año hace

Publicado

Accelerating Model Deployment in Financial Institutions with Automation

Today’s topic is one that’s really making waves in the financial world these days: speeding up the deployment of models...

más de 1 año hace

Publicado

Highlights from the MathWorks Finance Conference 2024

The 2024 MathWorks Finance Conference brought together industry leaders to explore the evolving landscape of finance...

más de 1 año hace

Publicado

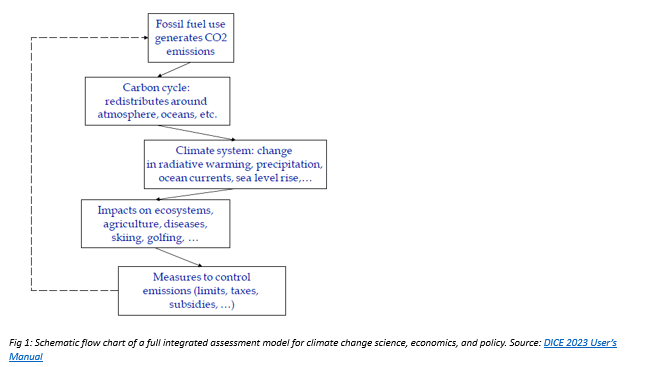

A MATLAB Implementation of the DICE-2023 Model for Climate-Economic Analysis

The DICE (Dynamic Integrated model of Climate and the Economy) model has been a cornerstone for understanding the intricate...

casi 2 años hace

Publicado

Trading Analysis in MATLAB using Python DataFrames

The following blog was written by Sara Galante, Senior Finance Application Engineer at Mathworks. The GitHub documentation...

casi 2 años hace

Publicado

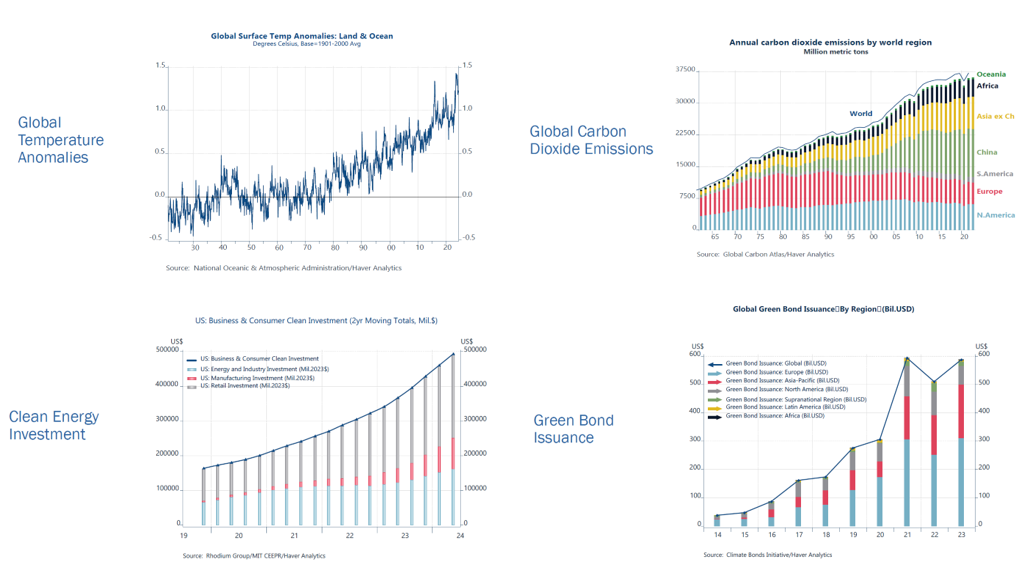

Modeling Carbon Emissions: An Econometric Approach

In a recent webinar hosted by MathWorks, we were joined by Andy Cates, a senior economist at Haver Analytics, one of our...

casi 2 años hace

Publicado

Deep Learning in Quantitative Finance: Multiagent Reinforcement Learning for Financial Trading

The following blog was written by Adam Peters, Software Engineer at Mathworks. Download the code for this example from...

alrededor de 2 años hace

Publicado

Key Insights from our Executive Panel Discussion: Addressing Climate Risk through effective Stress Testing, Reporting, and Governance

Background In the rapidly evolving landscape of financial risk management, addressing climate risk has emerged as a...

más de 2 años hace

Enviada

MATLAB Deep Learning Model Hub

Discover pretrained models for deep learning in MATLAB

más de 2 años hace | 4 descargas |

Publicado

MATLAB Portfolio Backtesting – A new app now on GitHub!

The following blog was written by Sara Galante, Senior Finance Application Engineer at Mathworks. MathWorks has a new...

más de 2 años hace

Publicado

Top MATLAB Quantitative Finance Resources now on GitHub

The following blog was written by Sara Galante, Senior Finance Application Engineer at Mathworks. MathWorks now has a...

más de 2 años hace

Publicado

Model Monitoring and Drift Detection with Modelscape

MathWorks recently hosted a webinar on Model Monitoring and Drift Detection, where Paul Peeling presented strategies for...

más de 2 años hace

Publicado

Deep Learning in Quantitative Finance: Transformer Networks for Time Series Prediction

The following blog was written by Owen Lloyd , a Penn State graduate who recently join the MathWorks Engineering...

más de 2 años hace

Publicado

Climate Risk in Finance: Insights from Our Comprehensive Executive Panel Discussion

The following blog was written by Arpit Narain from the MathWorks Finance team. 1. Introduction In today’s financial...

más de 2 años hace

Publicado

Managing and Fine-Tuning Portfolio Optimization Workflows with Experiment Manager

The following blog was written by Sara Galante, Senior Finance Application Engineer at Mathworks. The code used to develop...

más de 2 años hace