gevinv

Generalized extreme value inverse cumulative distribution function

Description

x = gevinv(p,k,mu,sigma)k,

location parameter mu, and scale parameter sigma,

evaluated at the probability values in p.

When k < 0, the GEV

distribution is the type III extreme value distribution. When k >

0, the GEV distribution is the type II (Frechet) extreme value

distribution. If w has a Weibull distribution, then –w has

a type III extreme value distribution and 1/w has a type II extreme value

distribution. In the limiting case as k approaches 0, the

GEV distribution is the mirror image of the type I (Gumbel) extreme value distribution. For more

information, see Generalized Extreme Value Distribution.

The mean of the GEV distribution is not finite when k ≥

1, and the variance is not finite when k ≥

1/2. The GEV distribution has positive density only for values of

x such that k*(x – mu)/sigma > –1. For more

information, see Generalized Extreme Value Distribution.

Examples

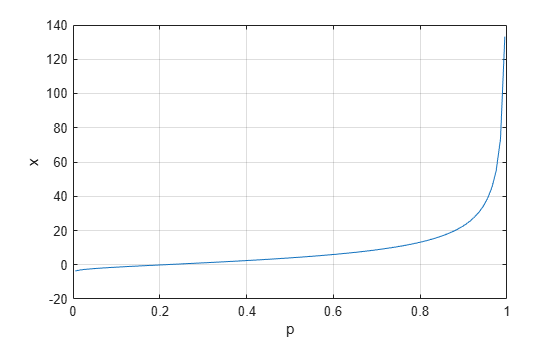

Compute the inverse cdf (icdf) values evaluated at the probability values in p for the generalized extreme value distribution with the shape parameter k, location parameter mu, and scale parameter sigma.

p = 0.005:0.01:0.995; k = 0.5; mu = 5; sigma = 2; x = gevinv(p,k,mu,sigma);

Plot the icdf.

plot(p,x) grid on xlabel("p"); ylabel("x");

Input Arguments

Output Arguments

Alternative Functionality

gevinvis a function specific to the generalized extreme value distribution. Statistics and Machine Learning Toolbox™ also offers the generic functionicdf, which supports various probability distributions. To useicdf, create aGeneralizedExtremeValueDistributionprobability distribution object and pass the object as an input argument or specify the probability distribution name and its parameters. Note that the distribution-specific functiongevinvis faster than the generic functionicdf.

References

[1] Embrechts, P., C. Klüppelberg, and T. Mikosch. Modelling Extremal Events for Insurance and Finance. New York: Springer, 1997.

[2] Kotz, S., and S. Nadarajah. Extreme Value Distributions: Theory and Applications. London: Imperial College Press, 2000.

Extended Capabilities

Version History

Introduced before R2006a